Choosing between hiring an employee or engaging an independent contractor is one of the most important decisions for Ontario businesses. The classification affects tax obligations, payroll costs, CRA compliance, and audit risk.

Many Ontario businesses face CRA reassessments and penalties due to worker misclassification. This guide explains the tax differences between employees and contractors in Ontario, how CRA determines status, and how to choose the right option in 2025.

Why Worker Classification Matters in Ontario

Incorrectly classifying a worker can result in:

CRA focuses heavily on employee vs contractor misclassification, especially in Ontario.

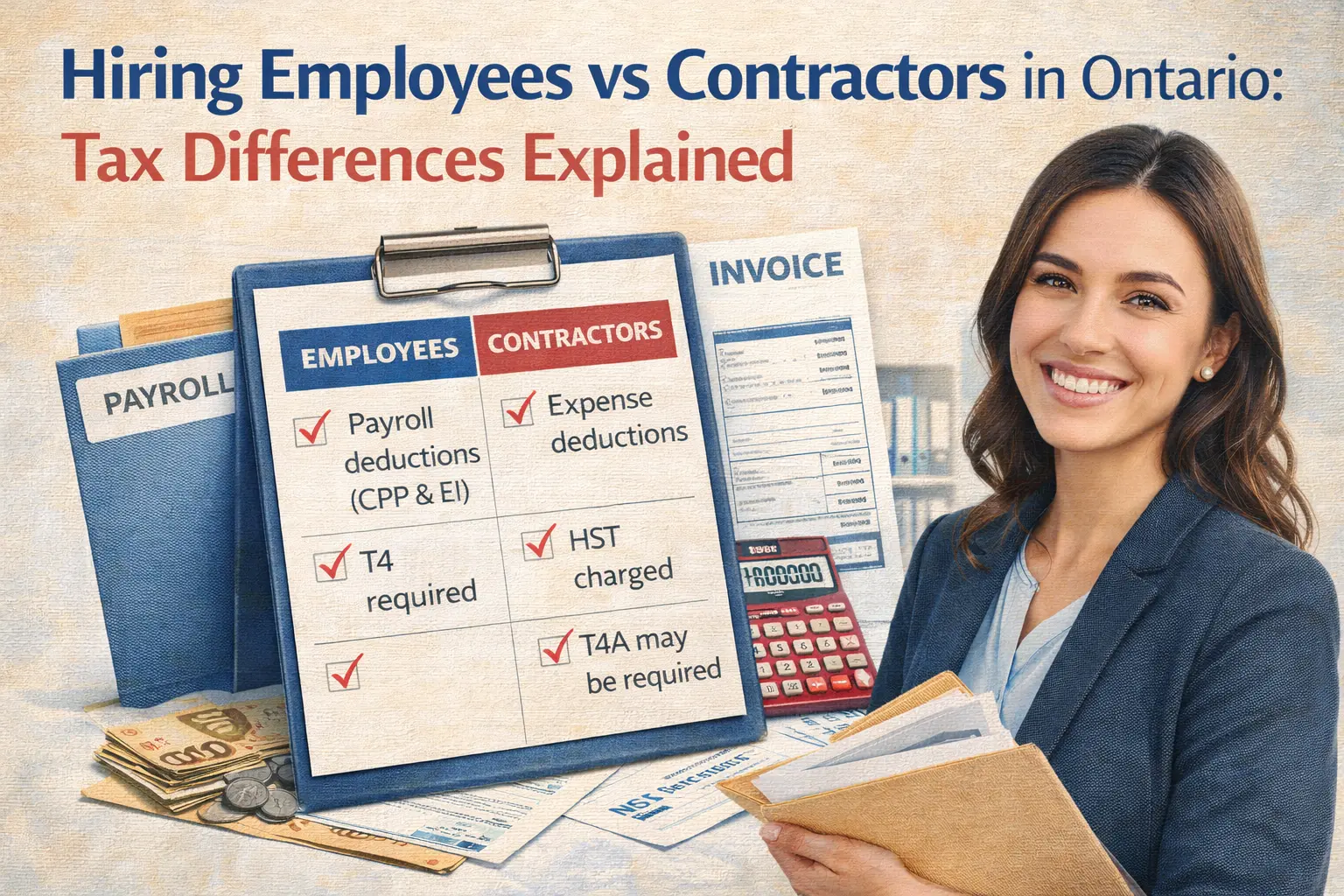

Key Tax Differences: Employees vs Contractors (Ontario)

Employees – Tax Treatment

When you hire an employee in Ontario, the business must:

Employees are generally more expensive from a payroll perspective.

Contractors – Tax Treatment

When you hire an independent contractor:

Contractors appear cheaper upfront—but misclassification risk is significant.

CRA Tests to Determine Employee vs Contractor Status

CRA looks at substance over form. Contracts alone are not decisive.

1. Control

2. Tools & Equipment

3. Chance of Profit & Risk of Loss

4. Integration

If CRA determines the worker is actually an employee, tax consequences apply retroactively.

Payroll Cost Comparison (Ontario)

Category

Employee

Contractor

CPP

Employer + Employee

Contractor pays both

EI

Employer + Employee

Not applicable

Payroll remittances

Required

Not required

T4 / T4A

T4 required

T4A may apply

CRA audit risk

Moderate

High if misclassified

HST Considerations in Ontario

Ontario businesses must verify contractor HST registration.

Common CRA Audit Triggers in Ontario

These scenarios often lead to CRA payroll audits.

How to Reduce CRA Risk

Proactive planning prevents costly corrections.

When Hiring an Employee Makes Sense

When Hiring a Contractor Makes Sense

How a CPA Helps Ontario Businesses

A CPA can:

Frequently Asked Questions (FAQs)

Can CRA reclassify a contractor as an employee?

Yes. CRA can reassess prior years and demand CPP, EI, penalties, and interest.

Do contractors charge HST in Ontario?

Yes, if they are registered and providing taxable services.

Is a written contract enough to prove contractor status?

No. CRA evaluates the actual working relationship, not just contracts.

Is hiring contractors cheaper than employees?

Not always. Misclassification penalties often outweigh short-term savings.

Should I consult a CPA before hiring?

Yes. Early advice prevents long-term CRA issues.